From the very beginning, the Founding Fathers believed that a strong republic depended on independent citizens who could stand on their own two feet. They spoke often about liberty, property, and the dignity of honest work.

Thomas Jefferson imagined a nation of landowners who answered to no king and relied on no distant power for their livelihood. James Madison understood that a wide base of property-owning citizens would guard against tyranny and protect self-government. The early American vision was built on the idea that ordinary people could work hard, own property, raise families, and shape their own future without depending on an elite class to carry them.

For generations, the middle class became the heart of that promise. It was the place where a steady job could support a home, a family could save for the future, and retirement felt like something secure. It represented stability, pride, and the belief that life could keep getting better with effort and responsibility.

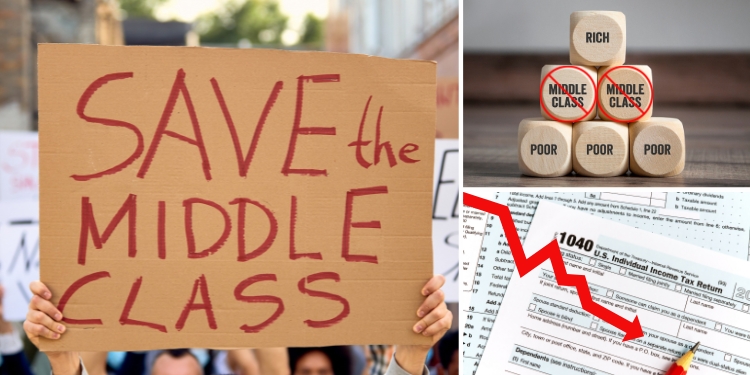

But something has changed. More Americans now feel that middle-class life is slipping out of reach. Recent polling shows that about two-thirds of voters believe a middle-class lifestyle is no longer affordable for most people, and many say it is harder to achieve than it was a decade ago. Rising costs, housing pressure, and a fragile sense of financial security have left families wondering what happened to the American Dream.

If you would rather just watch a video about it, here it is:

If you would prefer the text version, keep reading:

What People Really Mean When They Say “Middle Class”

The term “middle class” doesn’t have one precise definition, but it captures an idea most Americans understand from experience. When people say they are middle class, they usually mean they can afford a decent living, buy or own a home, pay for their children’s education, and build a cushion for the future. It is about stability and the ability to chart a steady course in life.

Beat the System! These Legal Loopholes Will Cut Your Bills by 80%

Even government statisticians and economic researchers use income ranges to describe middle-income households. Over time, these benchmarks help track how many families fall into that category.

What they found is that the share of Americans living in middle-income households has been shrinking. In the early 1970s, a strong majority fit within this range. Today, that share is noticeably smaller, and the portion of national income controlled by the middle class has fallen as well.

Rising Costs and Stagnant Wages

One of the central reasons families are feeling squeezed is the gap between what they earn and what they must pay. Over many years, prices for basic necessities have climbed faster than wages for most workers.

One of the central reasons families are feeling squeezed is the gap between what they earn and what they must pay. Over many years, prices for basic necessities have climbed faster than wages for most workers.

Houses that were once affordable with a modest income now command prices that require bigger loans, larger down payments, and stretched budgets.

Healthcare premiums and out-of-pocket medical costs have increased sharply, eating into the paychecks of working families.

In many communities, even necessities like food and transportation take up a larger share of family income than in the past. Economists describe this dynamic as a “middle-class squeeze,” where income growth for middle earners stagnates or grows slowly while costs in key areas rise rapidly.

When wages do not keep pace with inflation in everyday expenses, families must make hard choices: delay buying a home, take on more debt, postpone retirement savings, or cut into the resources needed for their children’s future.

Even when official statistics show some growth in household income over time, it is important to remember that these figures often lag behind the real cost of living in communities across the country. For many households, income gains are simply not enough to preserve the lifestyle they once had.

A Middle-Class Anchor Under Strain

At the core of the American middle-class identity has always been homeownership. Owning a home has meant more than shelter. It has been a source of savings, security, and a foundation for building wealth across generations.

In 1970, the median home price in the United States was about $23,000, while the median household income was close to $9,800. So, a typical home would cost a little more than twice a family’s yearly income.

Today, the gap has widened dramatically: the median home price is well over $400,000, while median household income is around $75,000. That means a typical home now costs five to six times what a household earns in a year.

Since 2000 alone, median home prices nationwide have risen by more than 150 percent, while median household incomes have increased by roughly 80 percent during the same period. In just the past few years, between 2020 and 2022, home prices jumped by nearly 40 percent in many parts of the country.

Young families and first-time buyers often find themselves priced out of the markets where they work and live, even with steady jobs and careful budgeting. Mortgage rates, property taxes, insurance costs, and maintenance expenses add even more weight to the monthly burden. What once felt achievable with discipline and patience now feels distant for many working Americans.

Even older homeowners who managed to buy decades ago feel the pressure in different ways. High property values can raise tax bills and insurance premiums, making it harder to stay put. At the same time, rising prices make downsizing complicated, since smaller homes are also expensive.

This shift could affect you and your family on many levels: job mobility, retirement planning, and the stability of communities that once depended on strong, long-term homeownership.

What Polls Really Say

A 2023 Federal Reserve Survey found that 37% of Americans could not cover a $400 emergency expense with cash, savings, or a credit card paid off at the next statement. Another 2025 study from Northwestern Mutual found that nearly 70 percent of Americans say financial uncertainty has made them feel anxious or depressed.

Here’s What an Economic Collapse Looks Like from the Inside

Those numbers point to something deeper than temporary frustration. When more than a third of the country cannot absorb a minor emergency, millions are living one broken transmission, one hospital visit, or one layoff away from financial collapse.

Poll after poll captures the same tension simmering under the surface: people feel exposed, stretched thin, and painfully aware that the margin for error has almost disappeared.

The Cost of Healthcare and Financial Stress

Healthcare costs are another heavy pressure on middle-class families. Premiums are higher than they were just a few years ago, deductibles have grown larger, and prescription prices continue to climb.

Healthcare costs are another heavy pressure on middle-class families. Premiums are higher than they were just a few years ago, deductibles have grown larger, and prescription prices continue to climb.

Even when you have insurance through your job, you could still find that medical bills still pile up when care is needed. Copays, lab fees, specialist visits, and unexpected charges add up quickly, often faster than paychecks can keep pace.

If you do not have strong employer coverage, the pressure is even heavier. A large part of your monthly income can disappear just to keep your family insured. That is money that could have gone toward savings, paying down debt, improving your home, or building something for the future (THIS will help you in a crisis!).

Add a serious illness or sudden accident, and everything gets thrown into chaos. What used to be a setback you could manage with savings can now turn into long-term debt. You may find yourself choosing between medical treatment and other basic needs, and that kind of choice chips away at the stability that the middle class once promised.

The Shift in Economic Opportunity

Over time, the economy has shifted in ways that have hit the middle class hard. Global competition, new technology, and changes in the labor market have reshaped work across the country.

Many industries that once provided steady, well-paying jobs without a degree have shrunk or moved overseas. Automation has boosted productivity, but wages have not always kept up.

At the same time, wealth at the very top has grown much faster than income for most households. This has widened the gap between the richest Americans and everyone else.

The Disappearing Middle Class

All of these trends hit regular Americans at the same time. Prices keep rising, wages move slowly, homes cost more than families can afford, and stable jobs disappear or change beyond recognition.

All of these trends hit regular Americans at the same time. Prices keep rising, wages move slowly, homes cost more than families can afford, and stable jobs disappear or change beyond recognition.

Meanwhile, those at the top keep pulling further ahead. The result is simple and painful: the middle class is not just struggling, it is shrinking.

That’s why more and more people feel like they are being pushed down while someone else benefits. Fewer Americans even call themselves middle class today, and many who still do admit they feel exposed.

Parents are no longer sure they can protect the life they built or hand it to their children. Surveys across the country show the same warning sign flashing again and again: people feel less secure, less stable, and less confident that the future will reward their effort the way it once did.

What Americans Want

Strip away the party labels and most Americans are asking for the same basic things. They want a house they can actually afford, a job that pays enough to live without constant stress, and healthcare that does not threaten to wipe out their savings. They want to work hard and see it mean something. They want to plan five or ten years ahead without feeling foolish for trying.

The Nightmare Scenario America Isn’t Ready For

Americans are not asking for luxury. A fair shot is enough. That’s what the ‘American Dream’ is all about, after all. Small businesses should be able to survive, local jobs should not vanish overnight, and rules should not crush ordinary families while powerful interests find ways around them. The economy should reward effort instead of connections, and the middle-class promise should feel real again, not like a story from the past.

So, if the middle class is disappearing, what should you do?

You do what Americans have always done when the ground starts shifting beneath them…

You stop waiting for someone else to fix it and take your family’s stability back into your own hands. Because that’s what this entire middle-class story has always been about.

For generations, middle-class stability meant having a cushion. It meant knowing that if the unexpected happened, you could handle it without everything falling apart.

Today, that cushion feels thinner.

If you feel the pressure tightening around the middle class, this is the moment to widen your margin again. Equip your household with the knowledge that keeps food on the table, water flowing, and leadership steady even if the grid fails tomorrow.

If you feel the pressure tightening around the middle class, this is the moment to widen your margin again. Equip your household with the knowledge that keeps food on the table, water flowing, and leadership steady even if the grid fails tomorrow.

Autopilot Homestead gives you everything you need to be prepared for what’s to come (and much more):

- How to have a thriving backyard

- Tricks to keep your livestock healthy

- How to secure dependable water sources near you

- DIY homesteading projects

- How to make your homestead bulletproof

In short, it focuses on practical steps ordinary families can apply quickly, without expensive gear or extreme measures, so that uncertainty no longer dictates your peace of mind.

If you sense that the safety net beneath the middle class is thinning, this is your opportunity to create your own.

Click here now to get Autopilot Homestead at the special price and make sure your family is ready before the next crisis hits.

A Crossroads for America

The idea that the middle class is disappearing is rooted in real economic pressures that Americans face every day. It is not simply a talking point, but a lived experience for many families who find that the costs of housing, healthcare, education, and everyday necessities stretch their budgets thinner than ever before.

At this moment, the United States stands at a crossroads. The path chosen in the coming years – through policies that expand opportunity, strengthen workers, and relieve the burdens on families – will shape whether the middle class regains solidity or continues to erode.

For a nation built on the belief that anyone can succeed with hard work, restoring a thriving middle class is not just an economic goal. It is a reaffirmation of who we are and what we hope to be.

You may also like:

What Is a Fiat Collapse and How This Might Affect Our Country (VIDEO)

Why Your Stockpile Might Be Doomed from Day One

What Happens If China Becomes The Ruling Economic Power Of The World

{kind=link}

MIGHT DISAPPEAR!? Hate top break the bad news to ya but it’s ALREADY gone.

Do your research and you’ll find that top 1% of Americans own 30% of the wealth, and the top 5% own the 70%, and the more you go the worst it gets, for educational purposes let’s stop at the 5% That means that the other 95% of Americans have to live with the 30% left.

If we make the numbers with 100 people and 100 dollars that means that 5 people own 70 dollars and the other 95 people have to divide the remaining 30 between them to live.

There was always a war, but not between democrats and republicans, woke and conservative, black and white, man and woman… the real war has always been between rich and poor.

They use all the above to divide people so we don’t see who the real enemy is, therefore we don’t fight the real war.

We never made a lot of money, instead we lived in old rent houses, wore old clothes, drove used cars, and took cheap vacations while we saved up money to buy our own place while also building a modest retirement account. The last five years of renting we actually lived in a shack on an old farm, the windows would blow out in a thunderstorm and the ceiling was a combination of popcorn and glitter. 25 years of doing without allowed us to spend the last 25 years in our beautiful little place in the country free of financial worries.

Ok, I get it that y’all need to sell stuff to keep this site going, but this well written article appears to simply describe your generalized optics and justification for promoting another printed item (sad to say but that’s been the trend here for the past couple years). Would have been a good place for a refresher of other ground-zero, tried and true common sense strategies: get out/stay out of debt; develop or improve career/trade skills that easily carry over into grid down living; develop subsistence skills to lessen budget needs (gardening etc); how to actually take stock of your strengths/abilities/limits; etc. I’m sure there are some basics out there that could fill a few pages. I see folks of all ages around who are struggling and needing direction, and often need a nudge to get off top dead center with realistic and attainable goals. Not everyone needs to buy/own a home (while this is the number one way to amass long term wealth). If pricing is out of reach now, and you’re in a good career path, renting is far more affordable than buying (avoids property taxes, preserves mobility if the opportunity to move/move-up presents itself, frees up personal time, limits repair costs …).

The premise of your article is that home ownership is/has rapidly slipped out of the reach of most Americans, but the product you are pitching relies on the requirement of already having a long term residence, on ehough land to grow a large garden/mini farm, raise livesstock, install water access, etc, etc. Quite a jump from the stark reality of non-ownership. Granted, many of the tips/techniques in the book(s) could apply to apartment living, but most may not.

Like above we did the same , lived modestly and paid our share

while the Thieves, Criminal, Politicians Stole our future , ssi,

gave to the invaders , demo thieves

and then created taxes to finish the elderly off , steal what they have

Then created covid Lies to finish off the past aged seniors

well Trump has arrived to stop the Crime Family s who run the politicians with

Money , wealth , Extortion

At the highest levels of societies ( Demo Dummies)

Thanks for the good Article Kate:

Some would say that we are headed toward a two-class society. Monarchy and Peasantry. This two-class society is often times identified with Socialism. There are certainly those who aspire for that type of Government. But keeping politics at a minimum I have found the following life strategy to be of some help.

1. If you are religiously inclined, get right with your God.

2. Get out of debt.

3. Become as self-sufficient as possible.

Number “1” above is obvious, but having established this will give you inspiration and hopefully a moral and honest path to follow through life. Good faith can be a great help and inspiration.

Number “2” although difficult to achieve is possible with the right life and income management. Even keeping debt below average can be a great help.

Number “3” again obvious, but the more you can do and provide for yourself the less you will be plagued by all the other woes mentioned in Kate’s article. r/Jeff

I have lead a pretty unplanned life … some college, but no degree, no real marketable trade, until I was 50, training in a field that was overly packed. Single most of my life, a working class schlub … I made ends meet, and saved what I could. At 60, I was making more money than I ever had in my entire life at $30k a year.

But I lived frugally … owning used cars most of my life. living in jeans and t-shirts, sneakers were 8 years old, when I replaced them. Early on, I bought some land … traded it as down payment on a house, and have refinanced that house more than a couple times … so at 66 I retired.

My house payment is under $800 a month, no car loans, no debt, 75 years old and a home value of $320k. Have a little precious metals in a safety deposit box .. have $25k cash there too … and about $60k in various bank accounts / CD’s. I buy what I want, but my needs are pretty simple … middle class? Who cares … it works for me.

lots of good points. YES we once worked and saved, but today, saving is now as , “well, this is the money I didnt get a chance to spend between paychecks, its called savings” !

30 years ago, we had nothing. I was MAD, at the grocery store every week we watched the cart in front of us, filled with what WE wanted, but could not afford. Then we watched them pay, with funny paper money, then plastic cards. It hurt watching my paycheck fund their groceries, the ones we had to go without. We would have had PLENTY of money, if it was not stolen from my pay and given to others. We had lots of friends, doing better than we were, every friday night, out to dinner they went. We saw others, more like us, but they spent their life complaining they had no money. They took home about 25% more than we did, out EVERY friday, and 1 or 2 more nights, newer car, etc.

We went without. Later, I discovered the wife had secretly run up 3 k in CC debt, then 5 K, then 10, then when I said good bye, she said here is another 13 K. The spending was just part of why i say good bye. 22 yrs later, I pay lots in property taxes, at multiple addresses. She owns nothing. She erns lots more now, she could pay that 400 $ but she cant handle unexpected 1 K. I can handle 400$ out of pocket, 25 K from a savings account, and buy an average house ( little over 300 K) with cash if I close a non retirement account. I learned how to save, spend ONLY what you MUST ! I said MUST. When you cant remember when you went to a restaurant last, your starting !

It adds up quick, when you stop feeling entitled !

37% cant handle 400$, Lets start by admitting that 37 % includes the POOR !

So, where do the Poor stop and Middle class start ?

Examine their spending habits, you will find miss management is why its 37 % that cant handle 400 $

First you save, then you spend, its how it works.

I am sorry, until you handle the self made POOR, you cant talk about how the middle class is disappearing. We would all like to become wealthy, but ask them to ONLY eat at home for 6 months, no coffee at drive thru, NO eating out, PERIOD. If they cant do that, they are self made POOR ! ! ! And Tuff $hit for them

Saving is a mind set … a friend of mine, is making in excess of $200k a year … and complains to me that with he and his wife working (she is a school teacher) … they can’t save $100 a month.

But she has CC debt of about $6k, they go out to eat 5 to 6 times a week … he goes to Starbucks for coffee, and a restaurant for lunch everyday, as does his wife. Their cars, are not more than 3 years old .. their home probably $500k.

When they applied for purchasing the house, he paid off her CC, and borrowed a couple thousand dollars from me, to put in a savings account making them look responsible. He and a friend now own a business, that in 2024 made $12m … and rubbing two nickels together would be difficult for him. He is considered middle class.

I know how to save, he can’t even get started. I eat out maybe once a month, including lunches, he goes out to eat probably 11 times a week. I could have $500 in my pocket, wearing 7 year old sneakers, and reason, I can’t buy new sneakers as I don’t have the money.